Payment fraud is costing subscription businesses more than they realize. According to industry data, merchants lose an average of $3.75 for every dollar of a fraudulent transaction. This is mainly due to due to chargeback fees and operational costs but for subscription-based businesses the damage runs even deeper. Payment fraud impacts customer lifetime value, brand reputation, and your ability to scale sustainably.

TL;DR: Key takeaways on payment fraud prevention

-

Shift to pre-authorization. The best anti-fraud strategy blocks fraud before it reaches the bank, protecting your authorization rates.

-

Balance is key. Aiming for "zero fraud" is unrealistic and costs your subscription business revenue. The goal is to balance security with conversion to maximize your payment success rate.

-

Fraud is a journey. Fraudsters attack the entire customer lifecycle, from free trial abuse to account takeovers, not just the checkout.

-

Automation scales. AI-driven fraud prevention is essential for handling traffic spikes (like live events) where manual reviews fail.

If you're leading a D2C subscription business, fraud prevention can't be an afterthought. It's a strategic imperative that directly affects your bottom line and growth trajectory. The question isn't whether fraud will target your business, but whether you're equipped to stop it before it drains your revenue.

Contents

- The real cost of payment fraud for subscription brands

- A new approach to payment fraud prevention: from reactive to proactive

- How to detect and prevent fraud: key strategies for subscription businesses

- How the right partner helps your fight fraud and grow

The real cost of payment fraud for subscription brands

Most business leaders understand that fraud results in chargebacks. What's less obvious is how fraud quietly erodes profitability across multiple dimensions and functions:

1. Financial drain

Every fraudulent transaction carries direct costs: chargeback fees typically range from $20 to $100 per dispute, and you lose the revenue from that transaction entirely. But indirect costs accumulate quickly.

Payment processors may increase your fees if your chargeback rate climbs above 1%. Persistent fraud issues can land you on a high-risk merchant list, making you subject to heavy penalties from VISA and MasterCard.

In fact, as of September 2025, these thresholds are even stricter. Visa now monitors a combined fraud and chargeback ratio, and businesses exceeding these new limits (chargebacks and fraud combined cannot exceed 1.5% of transactions for VISA, while the maximum chargeback rate for MasterCard is 1.5%) face significant penalties. Becoming a high-risk merchant also carries the risk of being banned from operating these key payment methods in specific countries.

For subscription businesses with recurring revenue models, the stakes are higher. A single fraudulent signup can result in multiple illegitimate payments, with the number of chargebacks dramatically growing over time.

2. Customer experience and churn

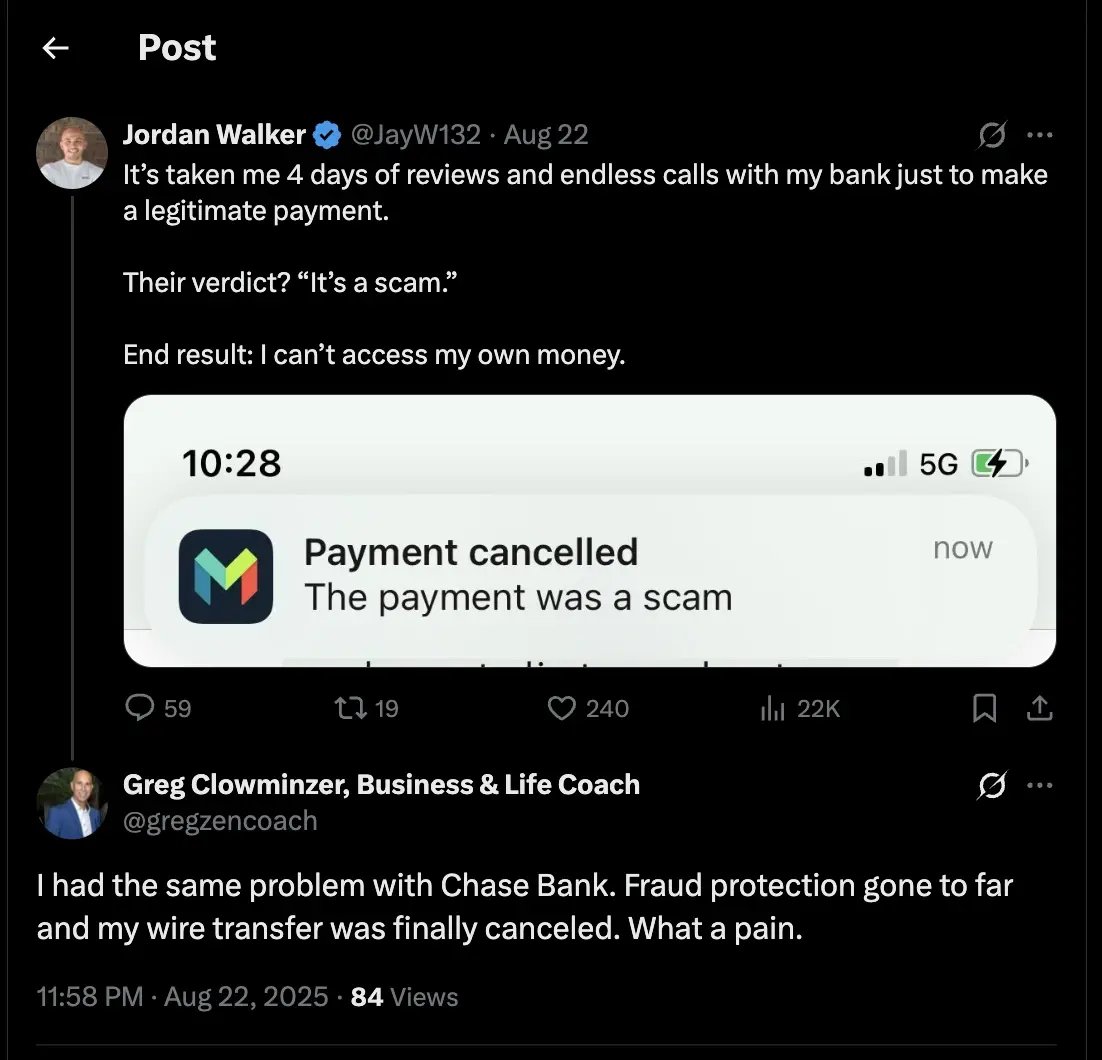

Overly aggressive fraud prevention creates its own problem: false positives. When legitimate customers have their transactions declined, they experience frustration that often leads to churn. Research shows that 27% of customers whose transactions are falsely declined will never attempt to purchase from that merchant again.

Two tweets illustrate a common frustration: legitimate transactions declined by overly aggressive fraud protection.

Account takeovers present another challenge. When fraudsters gain unauthorized access to subscriber accounts, it damages customer trust and loyalty, even though the legitimate buyer wasn't at fault.

3. Reputation damage

Repeated fraud incidents signal weak security to both customers and financial institutions. Customers may question whether their payment information is safe with you. Banks and payment processors may classify you as high-risk. This leads to increased scrutiny, higher fees, or even the termination of your merchant account.

For instance, this occurs when stolen credit cards are used by fraudsters who deploy bots to launch large-scale signup attempts. If these attempts succeed and payments go through, the resulting frustration can erode trust in your platform – both from customers and the banks involved.

From reactive to proactive: a new approach to payment fraud prevention

Traditional fraud management relied on reacting to chargebacks and manually reviewing suspicious transactions after they occurred. This approach is no longer sufficient.

High-performing subscription businesses now use pre-authorization fraud detection to identify and block fraudulent transactions before they reach issuers. This shift offers three major advantages:

-

Better authorization rates. By stopping fraud attempts before they hit issuing banks, you maintain a cleaner transaction history and avoid being flagged as high-risk.

-

Reduced operational burden. Automation eliminates the need for manual review queues, freeing your team to focus on growth rather than dispute management.

-

Improved customer experience. Legitimate customers move through checkout seamlessly without interfering with their bank, while fraudsters are quietly blocked in the background.

The most successful businesses treat fraud prevention as a competitive advantage. Unlike a commonly accepted idea, fraud prevention does not necessarily lead to a compromise in checkout experience. A smooth, secure checkout builds customer trust and increases conversion rates.

How to detect and prevent fraud: key strategies for subscriptions

Here are some key strategies to detect and prevent fraud in subscription businesses:

1. Leverage pre-authorization fraud screening

Fraud prevention should happen before transactions are sent for approval to the issuers, not by the issuing banks. Pre-authorization screening uses AI-driven risk models to evaluate transactions in real time and detect fraud patterns and trends. Leading companies like Cleeng provide real-time payment fraud monitoring.

Pre-authorization detection also includes reCAPTCHA, address verification, 3DS, and many others. Learn more about real-time fraud detection.

2. Understand fraud types common in subscriptions

Different types of fraud require different defenses. In the subscription space, the following are the most common types of fraud:

-

Card testing. Fraudsters make small transactions to validate stolen card numbers. These attempts often precede larger fraudulent purchases.

-

Free trial abuse. Bad actors create multiple fake accounts to exploit free trial access, particularly common in streaming and content platforms.

-

Account takeover. Stolen credentials allow fraudsters to hijack subscriber accounts and access premium content without paying.

-

Friendly fraud. Fraudsters dispute legitimate charges, claiming they didn't authorize a subscription or never used the service.

3. Automate payment fraud detection

Manual reviews don't scale. Streaming platforms and live event providers experience massive traffic spikes during major sports finals, concerts, or product launches. All pre-authorization security measure listed above are able to process thousands of transactions per second, clearing legitimate purchases instantly while flagging suspicious activity.

Automation also enables smarter 3D Secure routing. Instead of applying friction to every transaction, intelligent systems apply additional authentication only to borderline-risk cases, keeping checkout seamless for seemingly legitimate subscribers.

4. Balance security and conversion

Zero fraud is an unrealistic goal. The pursuit of zero fraud leads to false declines that hurt revenue more than fraud itself. Instead hoping for a total lack of fraud, aim for an acceptable fraud threshold that maximizes revenue while keeping losses within acceptable limits. This “risk appetite” is something that fraud prevention solution providers like Cleeng define and update over time, adapting it based on your current fraud exposure and other security measures like AI fraud tools.

A good practice is to monitor your payment success rate – the percentage of customers who successfully complete a purchase after attempting one. This metric balances fraud detection and prevention, authorization success, and customer experience. But here’s something important to remember: if your complete rate is declining, you may be blocking too many legitimate transactions!

With the Merchant Performance Dashboard, you get to keep a close eye on your payment success rate, a crucial metric used to fine-tune the fraud prevention thresholds effectively. The dashboard gives you a direct access to your payment analytics in real-time, delivering the clarity and control needed to improve the payment performance of your subscription business. See Merchant Performance dashboard demo.

Besides adapting risk thresholds over time, fraud rules and features and continuously tested through A/B testing and refined based on:

-

Geography (fraud patterns vary significantly across regions)

-

Customer type (new trial users vs. long-term subscribers)

-

Regulatory requirements (such as Strong Customer Authentication in Europe)

5. Protect the entire customer journey

Fraud doesn't only happen at checkout. Fraudsters exploit weak points throughout the customer lifecycle:

- Registration and login (credential stuffing attacks)

- Account management (unauthorized profile changes)

- Post-purchase actions (return fraud, coupon abuse)

A comprehensive fraud strategy covers every touchpoint, not just payment processing. It means implementing protective measures from the moment a customer first interacts with your brand. By monitoring and securing each stage, businesses can proactively detect and prevent fraudulent activities across the entire customer lifecycle, ensuring a robust defense against evolving threats.

How the right partner helps you fight fraud and grow

Managing fraud in-house requires significant resources: dedicated teams, advanced technology, and constant monitoring. For most subscription businesses, partnering with a platform that offers integrated fraud protection is the smarter path.

A subscription management platform with built-in fraud tools provides:

-

Revenue protection. Pre-authorization screening blocks fraud before it impacts your bottom line.

-

Reduced operational overhead. Automated fraud detection lets your team focus on growth initiatives rather than manual reviews.

-

Customer trust. A secure, frictionless experience keeps legitimate subscribers happy and engaged.

When evaluating partners, prioritize those that treat fraud prevention as part of a holistic payment strategy. Fraud and payments shouldn't be managed in silos – they're two sides of the same coin. The best solutions align fraud prevention with authorization success, ensuring that security measures don't inadvertently suppress conversion.

For example, Cleeng’s Merchant provides D2C brands with AI-driven anti-fraud tools, built-in security measures such as email verification and payment session throttling, as well as multi-layered risk settings whose performance is constantly monitored. This protects your revenue against emerging fraud threats with ease and efficiency. This results in Cleeng’s chargeback rate being less than half that of the industry (0.3% vs industry average of 0.8%), with brands like Jme reaching chargeback rates of 0.2%.

The industry average chargeback rate has been calculated by taking the average of the industry chargeback rates reported by Paykings (1%) and Clearly Payments (0.56%).

The industry average chargeback rate has been calculated by taking the average of the industry chargeback rates reported by Paykings (1%) and Clearly Payments (0.56%).

Fraud prevention enables growth

Protecting your subscription business from fraud isn't just about minimizing losses. It's about building a foundation for sustainable growth.

When you prevent fraud effectively, you maintain healthy relationships with payment processors, reduce operational costs, and create a seamless experience for your customers. You protect customer lifetime value and safeguard your brand reputation. Most importantly, you gain the freedom to scale without worrying that growth will expose you to unmanageable risk.

A smart fraud strategy is essential for thriving in the subscription economy. Ready to protect your revenue and build a more resilient subscription business? Talk to a Cleeng expert today or create your free Cleeng Pro account to see how you can get started with Cleeng in less than 60 minutes.

Frequently Asked Questions (FAQs) on Payment Fraud Prevention

-

What is online payment fraud and what is its real cost to a business?

Online payment fraud is any unauthorized or illegal transaction conducted by a fraudster. For a business, the cost is far greater than just the lost transaction. For every dollar lost to fraud, merchants often lose an additional $3.75 in chargeback fees, operational costs, and bank penalties. This doesn't include the damage to brand reputation and customer churn from false declines.

-

How does real-time payment fraud monitoring work?

Real-time payment monitoring works by using AI and machine learning to analyze hundreds of data points for each transaction before it is sent to the bank (this is called "pre-authorization"). In milliseconds, it assesses risk by looking at the user's device, location, and purchase behavior to decide whether to block the fraud attempt or approve the legitimate customer.

-

What are the most common types of fraud in the subscription industry?

The subscription industry faces unique fraud types, including:

-

Card testing: Fraudsters use small transactions to see if stolen credit card numbers are active.

-

Free trial abuse: Creating multiple fake accounts to repeatedly exploit free trial periods.

-

Account takeover (ATO): Using stolen credentials to hijack a legitimate subscriber's account.

-

Friendly fraud: A legitimate customer making a purchase and then disputing the charge with their bank, claiming it was unauthorized.

-

What are the most effective techniques to prevent online payment fraud?

The most effective strategy involves multiple layers:

-

Pre-authorization screening: Stopping fraud before it reaches the bank.

-

AI & automation: Using machine learning to detect patterns and scale protection during traffic spikes, which manual reviews cannot handle.

-

Unified strategy: Balancing security rules with customer conversion goals.

-

Journey-wide protection: Securing all touchpoints, including login and registration, not just the checkout.

-

How can a business prevent payment fraud without hurting customer conversion rates?

The goal is not "zero fraud," which leads to high "false positives" (blocking good customers) and lost revenue. The best approach is to find an acceptable fraud threshold that maximizes your payment success rate – the percentage of legitimate customers who successfully complete a purchase. This involves using smart, AI-driven tools that can tell a good customer from a fraudster, rather than blunt rules that block everyone.

-

Why is pre-authorization fraud detection so important?

Pre-authorization detection is critical because it blocks fraud before you are charged processing or chargeback fees. By filtering out fraudulent attempts before they reach the issuing banks, you maintain a cleaner transaction history. This signals to banks that you are a low-risk merchant, which leads to higher authorization rates for your legitimate recurring subscription payments.

-

What should a business look for in a payment fraud monitoring company?

Look for a partner, not just a tool. Your provider should offer an integrated solution that treats fraud and payments as part of one holistic strategy. Key features include AI-driven pre-authorization screening, automated tools that reduce your team's manual workload, and a clear focus on maximizing your overall payment success rate, not just blocking fraud. Cleeng is a great example of a trustworthy and efficient solution.